Latest images

Latest images

Pensacola Discussion Forum

This is a forum based out of Pensacola Florida.

Message [Page 1 of 1]

Message [Page 1 of 1]

Re: Chart of the Day ... 11/1/2013, 11:16 am

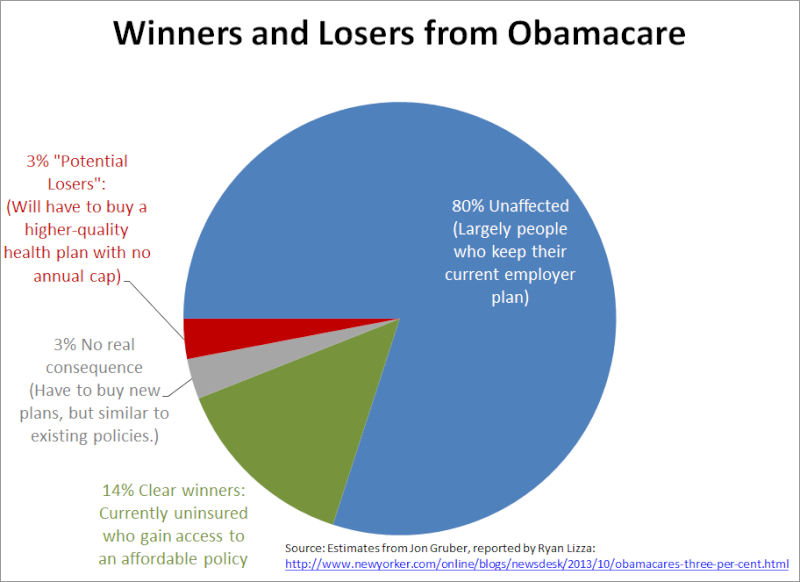

Obama Officials In 2010: 93 Million Americans Will Be Unable To Keep Their Health Plans Under ObamacareSal wrote:

Re: Chart of the Day ... 11/1/2013, 11:25 am

Good one, Bob.Bob wrote:Obama Officials In 2010: 93 Million Americans Will Be Unable To Keep Their Health Plans Under ObamacareSal wrote:

http://www.forbes.com/sites/theapothecary/2013/10/31/obama-officials-in-2010-93-million-americans-will-be-unable-to-keep-their-health-plans-under-obamacare/

So, according to the obama administration and your chart, that means 90 million is 20% of the population making the population of the United States be 450 million. I didn't realize that many more mexicans had crossed the border. I stand corrected.

Re: Chart of the Day ... 11/1/2013, 11:36 am Re: Chart of the Day ... 11/1/2013, 11:46 amThe health insurance policy I have now is the first and only insurance policy I've ever had. I've now had it for 35 years and I have never "gotten one of those letters".2seaoat wrote: Let the first person on this forum whose has never got one of these letters from an insurance company throw the first stone......there will be no stones thrown.

Re: Chart of the Day ... 11/1/2013, 12:05 pm Re: Chart of the Day ... 11/1/2013, 12:07 pm

Re: Chart of the Day ... 11/1/2013, 12:07 pm

2seaoat wrote:I am part of the eighty percent.

Re: Chart of the Day ... 11/1/2013, 12:12 pm Re: Chart of the Day ... 11/1/2013, 12:18 pm Re: Chart of the Day ... 11/1/2013, 12:23 pm Re: Chart of the Day ... 11/1/2013, 12:27 pm

But the pie chart doesn't show the segment I'm in. I'm in the segment that gets to keep my current insurance but have to bend over and take it up the ass or pay 200% of what I paid last year. Needless to say, I can't afford a 200% increase, so I've had to invest in lots of KY and Vaseline.Nekochan wrote:Read Sal's chart and believe what it says and everyone just Be Happy!

Re: Chart of the Day ... 11/1/2013, 12:29 pm Re: Chart of the Day ... 11/1/2013, 12:41 pm Re: Chart of the Day ... 11/1/2013, 8:36 pm

Re: Chart of the Day ... 11/1/2013, 8:36 pmBob wrote:

So, according to the obama administration and your chart, that means 90 million is 20% of the population making the population of the United States be 450 million. I didn't realize that many more mexicans had crossed the border. I stand corrected.

Re: Chart of the Day ... 11/1/2013, 9:03 pm

Re: Chart of the Day ... 11/1/2013, 9:03 pm

You should throw it at the jerks who sold you this subpar insurance...sorry, Bob. It will take time for this new law to make an impact...it may be (and I hope it is) that the current setup will not work as planned...and a lot of the reason for that is state-by-state obstruction...failure to set up a plan based around the new federal mandate...and yes, it is a mandate. The idea is that more people get coverage...it will take time for these people to enroll. The people in states like Florida will suffer because their leadership didn't want to provide anything for the general population...remember who donates to the GOP and especially the tea party. (Hint: It's not the labor unions.)Bob wrote:The health insurance policy I have now is the first and only insurance policy I've ever had. I've now had it for 35 years and I have never "gotten one of those letters".2seaoat wrote: Let the first person on this forum whose has never got one of these letters from an insurance company throw the first stone......there will be no stones thrown.

Where's my stone because I'll goddamn sure throw it.

Re: Chart of the Day ... 11/1/2013, 9:15 pmI already did. But fairy tales don't always have a happy ending.Floridatexan wrote:

You should throw it at the jerks who sold you this subpar insurance

Message [Page 1 of 1]

Similar topics

![]()

Permissions in this forum:

You cannot reply to topics in this forum

|

|

|